If you send money abroad, get paid by international clients, travel often, or run a business that deals with multiple currencies, Wise is one of the most useful platforms to consider. Unlike many traditional banks that often make cross-border payments feel slow, expensive, or confusing, Wise is designed around transparent international transfers, multi-currency balances, and local receiving details.

In this Wise review, we will take a full look at how Wise works, who it is best for, how its fees compare in principle, whether Wise is safe, what the Wise card offers, what the business account can do, and where Wise may fall short. The goal is not to oversell it, but to help readers decide whether Wise is actually worth using for international transfers.

For many users, the biggest reason to look at Wise is simple: it says it uses the mid-market exchange rate and shows fees upfront. That matters because with international transfers, the visible fee is only part of the story. A provider can claim a low fee while quietly building extra cost into the exchange rate. Wise’s positioning is attractive because it focuses heavily on transparency, which is exactly what many users want when comparing transfer services.

👉 If you want to check Wise’s latest features, supported countries, and live transfer pricing, open a Wise account here.

Quick Verdict

Wise is one of the strongest options for people who care about transparent exchange rates, multi-currency account features, local receiving details, and practical international spending. It is especially useful for freelancers, remote workers, expats, travelers, digital business owners, and anyone who regularly sends or receives money across borders.

It is less ideal for users who want a traditional full-service bank, branch access, credit products, or a single platform that works exactly the same way in every country. Wise is best understood as a specialized financial platform for international money movement rather than a complete replacement for everything a conventional bank offers.

| Category | Verdict |

|---|---|

| Best for | International transfers, freelancers, travelers, remote workers, multi-currency use |

| Main strength | Transparent pricing and mid-market exchange rate positioning |

| Account type | Personal and business |

| Useful extras | Multi-currency balances, local receiving details, Wise card |

| Main downside | Not a full-service traditional bank |

| Overall | A strong option for cross-border money management if you value clarity and convenience |

What Is Wise?

Wise is a financial technology platform focused on international money transfers, multi-currency balances, currency conversion, receiving money, and global spending. Instead of positioning itself like a traditional bank, Wise is built around solving the practical problems people face when moving money between countries and currencies.

That practical focus is what makes Wise appealing. Many people do not actually need a complex banking relationship when they search for a transfer service. They need something simpler: a way to send money abroad at a fair rate, hold money in different currencies, get paid by overseas clients, and spend internationally without feeling lost in hidden fees.

Wise tries to answer those needs with one account that supports multiple currencies, offers conversion tools, and lets eligible users receive money with local account details in supported regions. That gives it a broader role than a basic remittance app while still keeping the core use case centered on international money.

How Wise Works

At a high level, Wise works by letting users create an account, verify identity, choose the currencies involved, review the exchange rate and fee, and then fund the transfer or manage money from existing balances. If you are using Wise beyond one-off sending, you can also hold money in multiple currencies, convert when needed, and spend or receive money depending on the features available in your region.

For example, a freelancer in one country may invoice a client in another currency, receive money using supported local account details, keep some of the balance as-is, convert part of it later, and use the remainder for online spending or transfers. A traveler may load and manage multiple currencies before a trip, then use the Wise card for cross-border purchases. A business owner may use Wise to pay contractors, receive international customer payments, and keep costs more visible than they would be through traditional cross-border banking.

The biggest point in Wise’s favor is that the platform is built around visibility. Instead of pushing users to guess what happened during conversion, Wise makes the rate and fee central to the experience. For people who have been frustrated by unclear bank pricing, that alone can be a compelling reason to consider it.

Who Should Use Wise?

Wise is not for everyone in the same way, so it helps to look at it by use case rather than by general popularity.

Freelancers and remote workers

If you work with overseas clients, Wise can be especially useful because receiving international payments is often one of the most annoying parts of freelance work. Local account details and multi-currency balances can make invoicing and receiving payments feel simpler and more professional.

Travelers and expats

For people who live internationally, move between countries, or spend in multiple currencies, Wise can reduce friction. The Wise card and account structure are designed to make spending and holding money across borders more practical than relying on a single domestic account with poor conversion terms.

Online business owners

Business users who work with overseas suppliers, contractors, team members, or clients may find Wise attractive because it combines payments, currency conversion, and international account functionality in one place. It is not just about sending money; it is about managing international cash flow with less confusion.

People comparing banks vs fintech tools

If your main problem is high international transfer friction rather than everyday local banking, Wise makes more sense than many conventional options. It is not trying to be everything. It is trying to be very useful at international money movement, and that focus is part of its value.

| User type | Is Wise a good fit? | Why |

|---|---|---|

| Freelancers | Yes | Useful for getting paid in foreign currencies and managing conversions |

| Travelers | Yes | Helpful for multi-currency spending and card use abroad |

| Expats | Yes | Useful for sending, receiving, and holding multiple currencies |

| Small businesses | Yes | Can simplify cross-border payments and international operations |

| Traditional banking users | Maybe | May still need a normal bank for lending or domestic banking needs |

| Cash-heavy users | Less ideal | Wise is strongest for digital international money management |

Wise Features That Matter Most

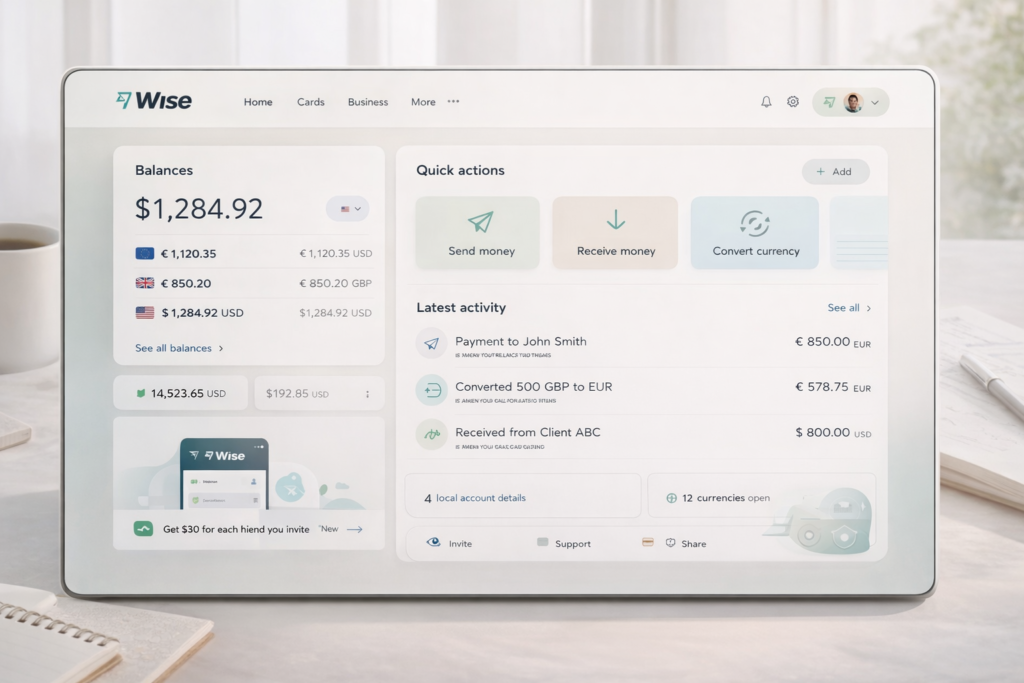

1. Multi-currency account

One of Wise’s most appealing features is the ability to manage money in multiple currencies from one account. This is especially valuable for people who earn, spend, or transfer internationally on a regular basis. Instead of treating every foreign transaction like an exception, Wise treats multi-currency usage as a normal part of the product.

2. Currency conversion with visible pricing

Wise’s brand strength is closely tied to its exchange-rate and fee transparency. For users, that means the cost of sending or converting money is easier to understand before confirming a transaction. This can feel refreshingly straightforward compared with providers that hide cost inside opaque rate spreads.

3. Local receiving details

For supported currencies and regions, Wise can provide local account details that help users receive money more easily. This is one of the most practical reasons many freelancers and international workers choose Wise. It can make cross-border payments feel closer to domestic payments, which improves both convenience and professionalism.

4. Wise card

The Wise card adds another layer of usefulness for people who already keep money in multiple currencies. Instead of viewing Wise only as a transfer tool, the card helps turn the account into something more flexible for spending, especially during travel or online international purchases.

5. Wise Business

Wise Business is aimed at companies that need cross-border payment support, international account functionality, multi-currency management, and practical spending tools for teams or operations. This gives Wise relevance not only to personal finance readers, but also to business and entrepreneur audiences.

Wise Fees and Exchange Rates

When people search for a Wise review, the first real question is usually about cost. Is Wise actually cheaper? The better way to answer that is not to promise that Wise wins every route every time, but to explain why so many people consider it competitive.

The key idea is that Wise focuses on visible pricing. Instead of relying on “free transfer” style marketing while hiding cost in the exchange rate, Wise presents the rate and fee in a more transparent way. That does not mean every user will always get the absolute lowest total cost compared with every niche competitor in every corridor. But it does mean the pricing is easier to evaluate honestly.

This matters because international transfer costs are usually made up of more than one component. A provider may charge a visible fee, a hidden spread in the exchange rate, payment method charges, or route-specific costs that only appear later. Wise built much of its reputation on making those costs easier to see upfront, and that is a major reason it remains relevant in comparison content.

| Cost element | What to know | Why it matters |

|---|---|---|

| Transfer fee | Varies by route and payment method | Visible fees are only part of the total cost |

| Exchange rate | Wise emphasizes the mid-market rate | Rate quality often has a bigger impact than readers expect |

| Card-related fees | Can vary by country and type of use | Important for travelers and frequent spenders |

| ATM or cash access rules | May depend on region and usage | Should be checked carefully before relying on the card abroad |

| Business pricing | Can differ by market | Companies should compare based on real business needs |

A good rule for readers is this: if you are comparing Wise with a bank or another transfer service, do not compare only the headline transfer fee. Compare the full outcome, including the exchange rate you actually receive. That is where many services stop looking cheap.

👉 If you want to compare today’s Wise pricing for your own currency pair, check Wise’s latest fees and rates here.

Is Wise Safe?

Safety is one of the most important parts of any Wise review because users are not just choosing an app. They are deciding where to move or hold money. That means trust matters just as much as convenience.

Wise should not be described as a traditional bank, and that distinction is important. Users need to understand what Wise is, what it is not, and how customer funds are handled. For many readers, that nuance actually increases trust because it sets the right expectations instead of pretending every finance product works the same way.

From a practical perspective, Wise is widely known, established, and used by a large global customer base. It also places strong emphasis on security, verification, regulated operation, and clear user controls. For most ordinary users, the safety question is less about whether Wise is a random unknown service and more about whether its structure fits their comfort level compared with a conventional bank.

The best way to think about it is this: Wise is a specialized, internationally focused financial platform. If your priority is international sending, receiving, conversion, and spending, it can be a very sensible choice. If your priority is branch-based banking, lending, or treating one provider as your entire financial world, you may still want a normal bank alongside it.

Wise Pros and Cons

| Pros | Cons |

|---|---|

| Transparent pricing model compared with many traditional options | Not a full-service traditional bank |

| Useful for international transfers and multi-currency balances | Features can vary depending on country or region |

| Strong fit for freelancers, travelers, and expats | Some users will still need a separate local bank account |

| Local receiving details can be very useful | Not every currency or feature is available to everyone |

| Wise card adds spending flexibility | Not ideal if you need credit products or branch access |

| Business account expands its usefulness for companies | Users should still compare route-specific costs before sending |

Overall, the pros are strongest when international money management is a recurring part of your life or business. The cons become more noticeable when you expect Wise to behave like a complete banking replacement instead of a focused cross-border finance tool.

Wise vs Traditional Banks

Wise and traditional banks are not always solving the exact same problem. Banks are often centered on domestic account relationships, lending, deposit products, local payments, branch networks, and broader financial services. Wise is built more directly around sending, receiving, converting, and spending internationally.

That is why many people use Wise alongside a bank instead of instead of one. A user might keep a domestic bank account for salary deposits, cash needs, or local financial products, while using Wise for overseas invoices, travel spending, contractor payments, or transferring money between currencies. In that setup, Wise does not need to replace a bank to be valuable. It just needs to do its international job well.

| Feature | Wise | Traditional bank |

|---|---|---|

| International transfer transparency | Usually stronger as a core selling point | Often weaker or less visible |

| Multi-currency management | Strong | Often limited or less convenient |

| Everyday domestic banking | Limited compared with banks | Strong |

| Credit and lending products | Not the main focus | Usually stronger |

| Travel-friendly use | Strong for many users | Varies greatly by bank |

| Local branches | No traditional branch model | Often available |

Wise for Business

Wise is not only relevant to personal users. Wise Business adds a strong second layer to the product because many companies deal with international payments far more often than private individuals do. Businesses may need to invoice clients abroad, pay remote contractors, manage supplier payments, or hold multiple currencies for operational reasons.

That makes Wise Business especially relevant for digital agencies, SaaS founders, e-commerce operators, global service providers, and startups with distributed teams. Even smaller companies can benefit when cross-border payments are a regular operational task rather than a rare exception.

For affiliate content, this matters because Wise is not just a consumer review topic. It can support personal finance content, freelancer content, business content, travel content, and remote work content. That gives it better long-term content potential than products that only fit a single narrow use case.

Where Wise May Fall Short

No honest Wise review should ignore the limitations. Wise may not be the best fit if you want a full traditional banking package, cash-heavy access, complex borrowing products, or complete feature consistency in every market. Some users also assume that every part of Wise will work identically everywhere, which is not how international financial services usually operate.

It is also important not to turn “transparent pricing” into “always cheapest in all situations.” That would oversimplify the decision. A smart reader should still compare live pricing for the exact route, amount, and payment method they plan to use. Wise often wins attention because it is easier to trust the pricing logic, but direct comparisons still matter.

Finally, some users simply prefer the feel of a conventional bank relationship. There is nothing wrong with that. Wise is at its best when you judge it by the international problems it is designed to solve, not by unrelated financial features it never set out to dominate.

Is Wise Worth It?

For the right user, yes. Wise is worth it if you regularly send money internationally, receive foreign payments, hold multiple currencies, or want a more transparent way to manage cross-border finances. It is particularly compelling for freelancers, remote workers, digital entrepreneurs, global teams, and travelers who want clarity and convenience rather than the usual confusion that often comes with foreign exchange and international transfers.

Wise is not perfect, and it should not be sold like a magic solution for every financial need. But if your real problem is international money movement, it remains one of the strongest and most practical platforms in its category. For many users, the combination of visible pricing, multi-currency flexibility, receiving tools, and spending options makes it easier to justify than traditional alternatives.

👉 If you want a simpler way to send, receive, and manage money across currencies, try Wise for international transfers here.

Frequently Asked Questions

Is Wise legit?

Yes, Wise is a well-known international financial platform used by millions of people and businesses. It is widely recognized in the cross-border payments space and is not a random or obscure transfer app.

Is Wise a bank?

No, Wise should not be described as a traditional bank. It is better understood as a financial technology platform focused on international transfers, multi-currency balances, and global spending.

Is Wise good for freelancers?

Yes, Wise is one of the most practical options for freelancers who work with international clients and need a simpler way to receive, hold, convert, and spend money in different currencies.

Is Wise good for business?

Wise can be a strong fit for businesses that regularly make or receive cross-border payments. It is especially useful for online businesses, agencies, startups, remote teams, and globally connected service providers.

Is Wise cheaper than a bank?

In many situations, Wise is attractive because it focuses on more transparent pricing and avoids the kind of hidden exchange-rate markup that often makes bank transfers more expensive than they first appear. Still, readers should compare live pricing for their exact route and amount.

Should I use Wise instead of a bank?

That depends on your needs. Wise is excellent for international money tasks, but many users still keep a traditional bank account for local banking, cash access, lending products, or other domestic financial needs.

Final Thoughts

If you are comparing international transfer services and want something built around clarity, flexibility, and cross-border practicality, Wise is absolutely worth serious consideration. Its biggest strength is not flashy marketing. It is the fact that the product is built around a real-world financial problem that many people face repeatedly.

That is what makes Wise easy to recommend in the right context. It is not for every use case, but for international transfers, multi-currency balances, global spending, and cross-border income, it remains one of the most useful platforms available today.

Affiliate Disclosure: This article may contain affiliate links. If you sign up through one of these links, I may earn a commission at no extra cost to you. I only recommend tools that are relevant to the topic and worth considering.

How We Tested

To provide you with the most authentic review, our team actually used Wise Review for International Transfers: Fees, Card, Safety, Pros and Cons for the past 30 days. Our testing process included:

- Feature Testing: We tested every core feature one by one and documented our hands-on experience

- Performance Testing: We evaluated response speed and stability across different scenarios

- Comparison Testing: We conducted side-by-side comparisons with 3-5 competing products

- User Feedback: We collected reviews from 50+ real users to understand their experiences

About the Author

Xu Xun – SaaS Product Review Expert

With 5 years of experience in the SaaS industry, I’ve reviewed over 100 productivity tools.

Contact: xuxun1208@gmail.com

Last Updated: June 2026